Click HERE to read the original article on Medium.com

Is a Donor Advised Fund (DAF) right for me?

William B. Burns, Jr., CFP®

Aug 27

You are probably familiar with “Christmas Club” accounts — a dedicated savings account made popular in the 1960s and 1970s for you to fund throughout the year so you have money to spend for holiday shopping. You may have even established other special savings accounts in the past, such as a “vacation account” or a “new car account”. Think of a Donor Advised Fund as a personal “charitable gift” savings account. You can set money aside in this special account for use down-the-road.

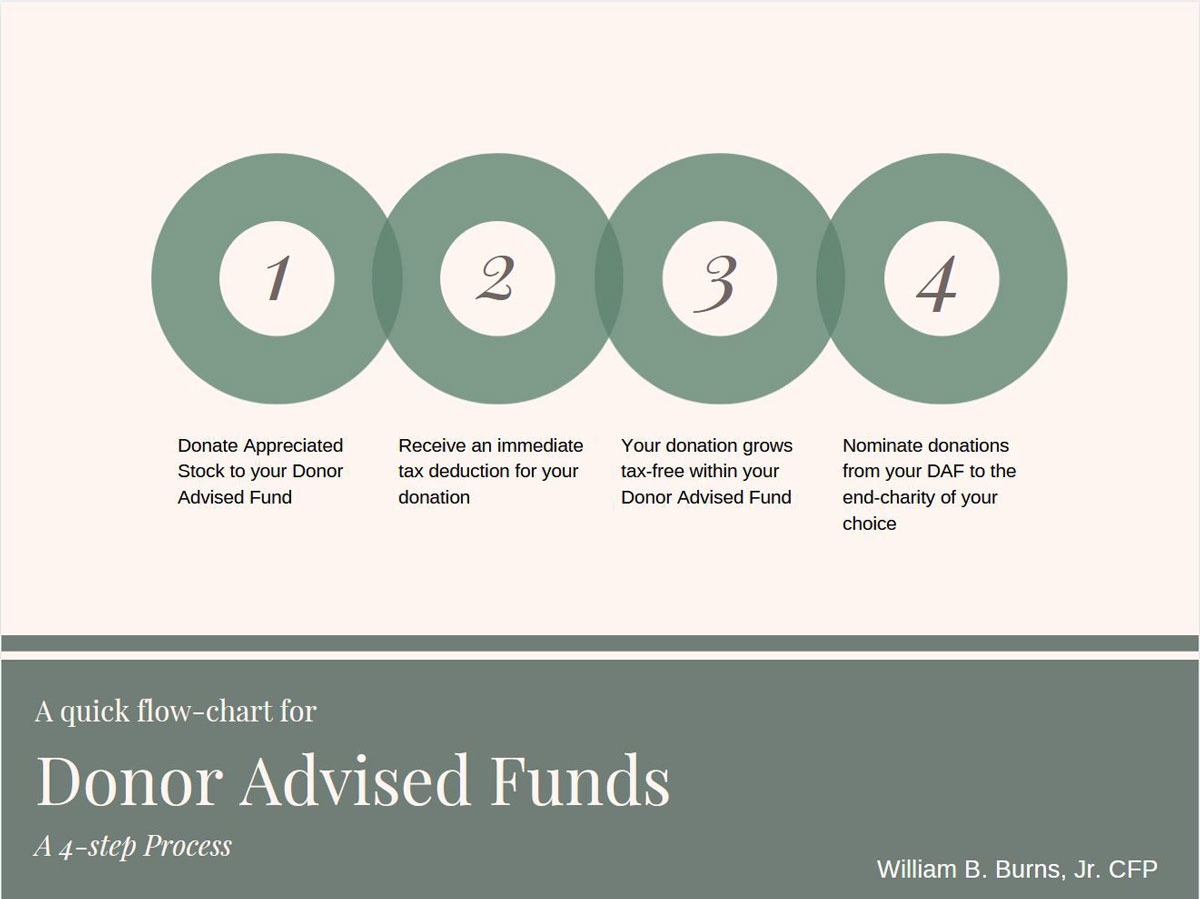

A Donor Advised Fund (DAF) is established by a non-profit organization, and Donors make an irrevocable gift into the DAF, to ultimately be distributed to an end-charity. Since the fund itself is registered as a charity, donors receive an immediate tax deduction for their contribution, even if it is not distributed to an end-charity until a later date. While the money is in the DAF, the donor has the ability to invest that money in a variety of mutual funds or other investments, and if the account value grows, the donor can gift the profits to end charities as well. Of course, if the account value falls, then the donor will have less to gift to the end charities.

The tax deduction received by the donor is based on the value of the donation on the day it is made to the DAF, so future appreciation (or depreciation) does not influence the tax deduction.

Three of the largest sponsors of Donor Advised Funds are: Charles Schwab, Fidelity, and Vanguard.

So what are the benefits of a DAF?

- You get an immediate tax deduction for gifts to the DAF, even if you choose to not have them distributed to an end-charity right away. You could make a gift to the DAF today, and perhaps allow it to grow over the next decade before making a grant to the end-charity (subject to any accumulation rules of the fund).

- You can gift appreciated stock to the DAF, eliminating a future capital gain from your portfolio. Lets suppose you purchased shares of XYZ stock 10 years ago at $100 per share, and today that stock is trading at $200 per share. You purchased $10,000 worth of stock that is now worth $20,000. If you were to gift the $20,000 of stock to the DAF, not only do you get the tax deduction, you also eliminate a future $10,000 capital gain from your portfolio. Your DAF will sell the stock — not you — so you will not be subjected to any capital gains taxes.

Assets held within a Donor Advised Fund are not subject to any Estate Taxes at your passing. - Assets held within a Donor Advised Fund can be invested and future growth will be tax-free.

- The internal investment expenses of the Donor Advised Funds are usually quite low, and significantly less expensive than establishing your own private foundation.

- You can provide a custom name for your Donor Advised Fund, such as “The John and Sally Smith Charitable Fund”.

Donor Advised Funds — Burns Matteson Capital Management

Why wouldn’t I just give directly to a charity?

- Some charities are not able to accept gifts of appreciated stock like a DAF can.

- With some charities, you might like to provide support to them over multiple years. Rather than give money to the charity all up-front, you can donate the money to your DAF, and then have the DAF distribute it to the charity over a period of months or years.

- Sometimes you might like to donate anonymously to a charity. With a DAF, you can request that your name be withheld from the end-charity.

What are the downsides?

- Your gift to the DAF is irrevocable. Once you make a gift to the DAF, you no longer control the money. Your role becomes one of a “nominator”, instructing the DAF whom to distribute the money to, and on what schedule.

- Because you are a nominator, and not the owner, there is always a risk that the DAF denies your request to support a particular charity. In my experience with these funds I have never seen that happen as long as you are requesting a gift to a registered 501(c)(3) charity, but if you wanted to support a brand new charity, I would suggest speaking with the DAF sponsor to get them “approved” before making your contribution to the DAF.

- This is not meant to be an all-inclusive list, so please make sure you speak directly with the DAF sponsor before making a financial commitment. In addition, nothing contained in this article should be construed as tax advice. Please make sure to consult your own tax preparer/advisor before making any financial commitments.

Real Life Stories:

We’ve assisted many clients with Donor Advised Funds over the past decade. Here are three real-life scenarios where the funds have been useful:

- Accelerated gift in a big tax year: We had a client a few years ago who received a substantial seven figure bonus. Knowing that he would have a big tax bill that year, we placed several hundred thousand dollars in a Donor Advised Fund before the end of the year. The client received an immediate tax deduction, and he “pre-funded” his charitable donations for many years to come.

- Accelerated gift before tax law changes: When it became clear that Washington was going to reduce the federal tax rates in 2018, we had many clients who made accelerated gifts to a Donor Advised Fund in the fall of 2017. For tax year 2017, their highest federal tax bracket was 39.6%, but in 2018 that fell to 37%. By making a larger charitable contribution in 2017, their deduction was worth an additional 2.6% tax savings.

- Auto Pilot for Snowbirds: We have many clients who travel south for the winter, but they wish to continue supporting their local church on a month-to-month basis. Rather than have the burden of mailing checks in the winter months, or making annual contributions to their church, a Donor Advised Fund can mail a check for a predetermined amount every month (or even every week). A donor can make an annual gift of stock to the DAF, and then the DAF can send out a regular donation to your end-charity on the schedule you have selected.

Get the family involved:

In my last article I asked the question of “what makes you YOU”, discussing the desire many families have to pass on more than just their financial wealth. One of the greatest assets you can pass along to the next generation is your charitable mindset.

By using a Donor Advised Fund you can purposely gift more to the fund than what you plan to distribute in the current year. This allows you to accumulate a balance in the fund, growing tax-free, to be used for larger and more impactful gifts down-the-road. You can also name your children as a “successor nominator” on your DAF, so at your passing they can continue to carry out your charitable legacy.

If you do not have children, you can provide legacy instructions to the DAF sponsor for them to continue to support certain charities after your passing.

In my last article I discussed the benefit of providing charitable “gift certificates” to your children. Parents have the opportunity to get their children involved with their Donor Advised Fund, allowing the children to select some of the charities that you support.

I’ve personally used a Donor Advisor Fund for more than a decade, and I’ve been very happy with the ease of administration and the ability to get our family more involved with our charitable contributions.

About the author

William B. Burns, Jr. CFP® is a CERTIFIED FINANCIAL PLANNER professional and President of Burns Matteson Capital Management, a Financial Planning and Investment Advisory Firm with clients throughout the United States. He helps high-net-worth families reduce the worry and anxiety sometimes associated with wealth, allowing families to reclaim that time to reinvest back into their family, social, and professional relationships.

Eric Sweet, FPQP®

Eric Sweet, FPQP® Nathan R. Burns, MBA

Nathan R. Burns, MBA Christopher Davis, CFP®

Christopher Davis, CFP® Kelley Zimmerman, FPQP®

Kelley Zimmerman, FPQP® William B. Burns JR., CLU, ChFC, REBC, CFP®

William B. Burns JR., CLU, ChFC, REBC, CFP® William F. Redder

William F. Redder